It’s easy to forget about self-care during finals week, but that doesn’t mean you should put it on hold. Taking care of yourself keeps you sane and it helps you stay energetic and focused enough to do well on your exams. Here are a few tips to follow.

Exercise

We already know that physical activity reduces stress and anxiety, but it may do even more than that. A recent study found that people who exercised a few hours after learning new information were more likely to remember it than those who didn’t exercise. Try boosting your brain and make time to go for a walk, attend a fitness class, or play your favorite sport.

If you’re really short on time, you could also bring your notes to the gym and study while you’re on the elliptical machine or exercise bike. Need motivation? Find a workout buddy; it’s easier to get your butt in gear when someone else is counting on you.

Indulge Yourself

Look, you’re a human being — not a study machine. Whatever it is you’re dying to do, make time for it. Change out of those sweatpants and have an extra-long shower. Paint your toenails. Doodle in your sketchbook or talk on the phone with a friend. Heck, blast your music and dance around in your underwear if it’ll make you feel better. It’s important to do well on your exams, but it shouldn’t cost you your sanity.

Eat Properly

When you’re short on time, it’s tempting to just eat ramen noodles and call it a meal. It’s fine to do that sometimes, but you really should get in some healthy meals. Getting enough nutrients keeps your energy up and keeps your immune system strong. Let that slip too much, and you’re susceptible to colds and other viruses. Studying is horrible when you need to blow your nose every two minutes.

Ideally, you should cook a meal that includes vegetables. If that feels like too much work, pick up some healthy snacks. There are plenty of inexpensive, ready-to-eat foods such as apples, bananas, crackers and peanut butter, yogurt, or baby carrots and hummus.

Get Enough Sleep

This may seem like an impossible task, but it’s really important to get enough sleep. Many students don’t get enough shut-eye, which leads to decreased concentration, memory, and overall performance. Clearly, this doesn’t do much to help you when you’re trying to memorize several months’ worth of notes.

It’s better to get a full night of rest, but if that all-night cramming session is unavailable, you should try napping. Naps can’t compensate for inadequate sleep, but they’ll make you feel more alert. Keep your nap between 20 and 30 minutes, and you’ll wake up feeling refreshed. To boost your memory and creativity, try sleeping for 90 minutes; this is enough time to complete a full sleep cycle. Anything between 30 to 60 minutes, however, will make you feel worse.

Finals week is so hectic that you probably feel like all you do is study. Change that feeling by following at least one of these self-care tips. You’ll feel better, and you’ll probably remember your notes better too.

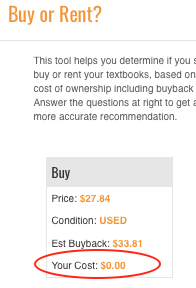

What’s total cost of ownership? That’s what it costs you to get the book and use it, whether that’s buying it and selling it back or renting it and returning it. Sometimes it’s cheaper to rent, sometimes it’s cheaper to buy and sell back, and now you can know and make smart money decisions rather than guess and take a costly hit.

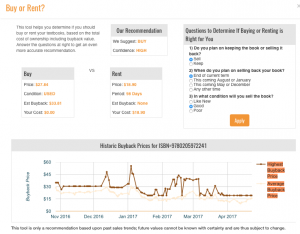

What’s total cost of ownership? That’s what it costs you to get the book and use it, whether that’s buying it and selling it back or renting it and returning it. Sometimes it’s cheaper to rent, sometimes it’s cheaper to buy and sell back, and now you can know and make smart money decisions rather than guess and take a costly hit.